ECONOMY

While we remain optimistic about global economic growth in 2025, we believe that the Fed’s path of rates is highly uncertain. We expect more inflationary pressures and market volatility under President Trump. A few themes that we will be monitoring: 1) Energy Transition— we think there will be a decrease in federal funding for renewable energy. The longer the energy transition takes, the more expensive it will be. 2) Shift from “Benign Globalization” to “Great Power Competition”. There is potential for a 10% tariff on all US imports, 60% tariff on Chinese exports. We would expect onshoring of US businesses to continue, which could be inflationary in the near term. 3) The Great Labor Rebalance—with more constraints on immigration, we would expect labor shortages to continue, which puts upward pressure on wage inflation. Potential risks on the horizon include geopolitical escalation and tariffs that are too effective which could hurt GDP growth. One outlier we need to monitor is how effective Elon Musk’s DOGE will be in cutting US spending.

EQUITIES

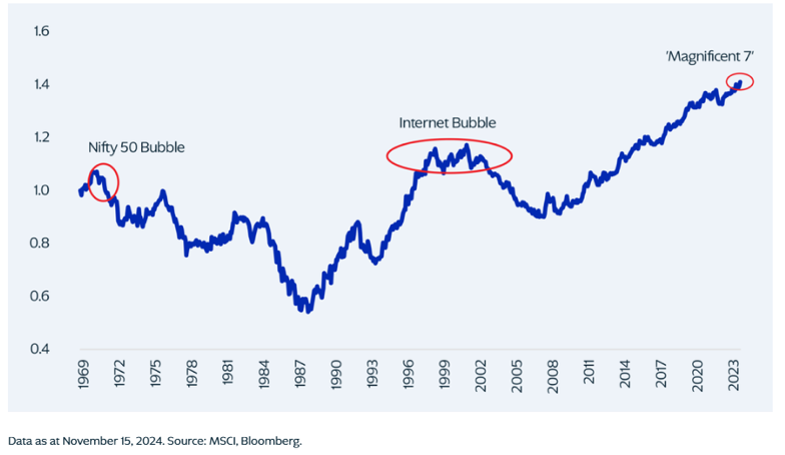

U.S. equity indices registered stellar gains for 2024, with the S&P 500 Index up by 25% for the year propelled by a narrow group of large technology stocks, leaving stable stocks out of favor2. The returns for other major equity benchmarks spanned a wide range, with the Dow Jones Industrial average up 15%, the equal weighted S&P 500 Index gaining 13%, U.S. small capitalization stocks increasing 12%, and international stocks as measured by the EAFE Index up only 4%2. Corporate profit growth of more than 10% and expectations of interest rate cuts by the Fed underpinned gains in stocks2.

The US market believes that it has the macro picture figured out as it has priced in a pro-growth with benign risk forecast for 2025. Our base case is for resilient growth in the first half of 2025, and a weaker second half of the year as visibility weakens. Our thesis rests on that there are two “puts” in place, a Federal Reserve that is easing financial conditions and President that is pro-growth. We believe we are in the later parts of this cycle; we want to position portfolios for cyclical tilt, but we do not want to abandon the big cash producers of the “Mag 7”.

Relative Performance of U.S. Equities vs. Global Equities

FIXED INCOME

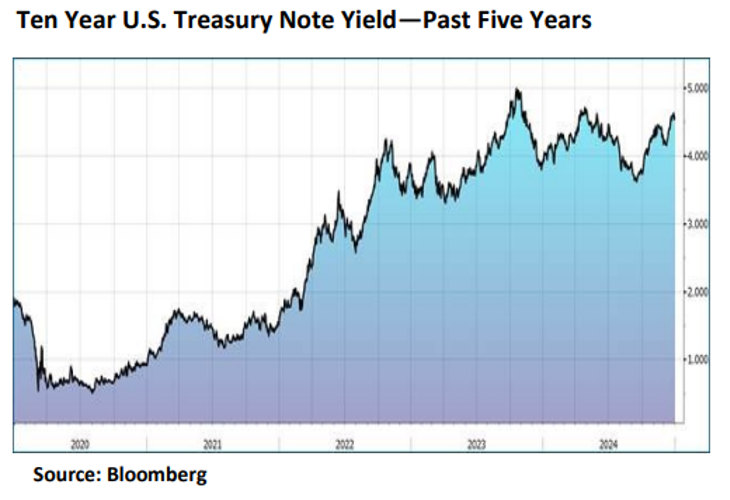

Bond yields have surged in the last part of 2024, we believe it is a great time to rebalance portfolios from the pricey stock market and reinvest in bonds where we can lock in these higher yields. We would not be surprised if the bond market outperforms the stock market in 2025. Areas we favor are investment grade corporates with medium duration, and municipal bonds.

ALTERNATIVES

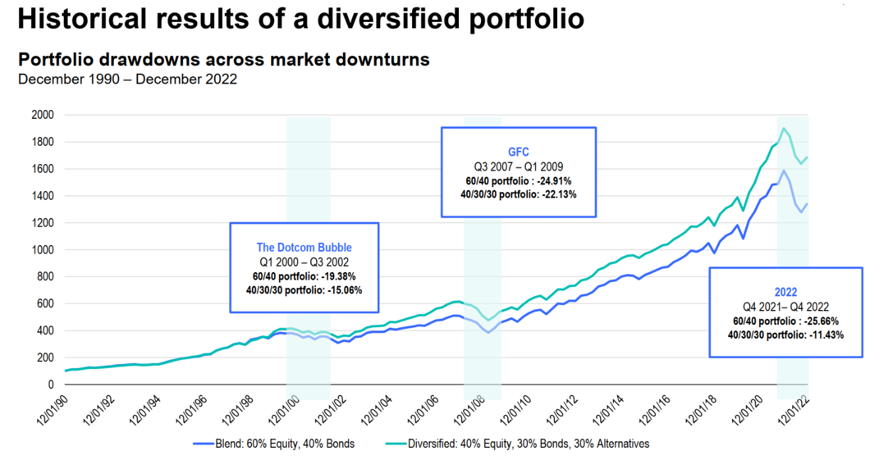

President Trump’s victory has pushed us to double down on our conviction of increased inflation volatility. Regardless of the path of U.S. rates, elevated inflation volatility is driving a higher correlation between stocks and bonds, compelling investors to find diversification elsewhere. We believe this period will be an opportune time to adjust portfolio construction and lean into private markets. Over the past 10 years, 60% stock / 40% bond portfolio returned an average of ~8%3. To achieve that return over the next five years amid elevated inflation, higher borrowing costs, and slower real economic growth, investors may need to diversify into alternative asset classes such as private credit, private equity, and infrastructure. The advantage of rebalancing with a tilt towards alternatives is to increase returns, generate income, and reduce volatility.