A Difficult Start to the Year

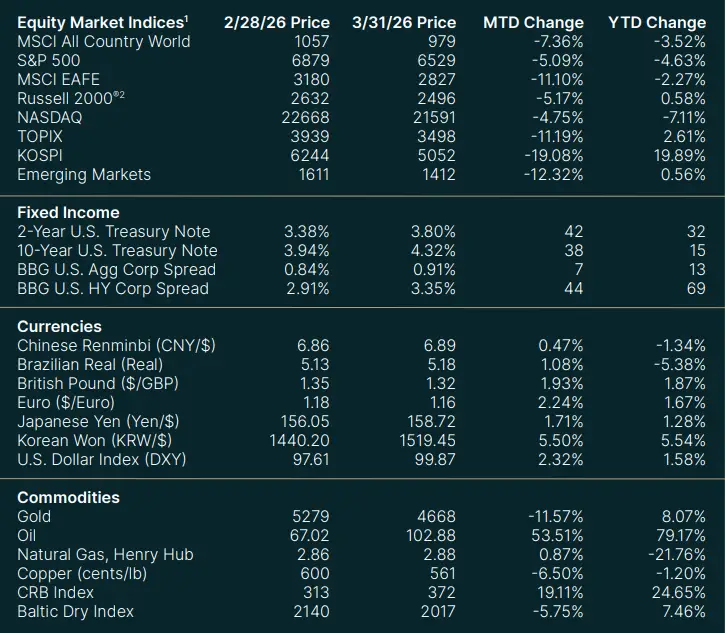

The first quarter of 2026 was a rough stretch for investors. AI-related disruption and the February 28th strike on Iran combined to produce the worst first-quarter performance since 2022. The S&P 500 finished the quarter down -4.6%, and there were few places to hide — bonds declined -0.5% as well1.

With so much uncertainty surrounding the conflict in Iran, sharp market swings are likely to continue. The current disruption is far more severe than the 1970s energy crisis, which affected roughly 7% of the world’s energy supply compared to 20% today2. Until there is a resolution to the Iran conflict, elevated oil prices make it difficult for stocks to mount a lasting recovery. Higher oil prices also create problems for the Federal Reserve and central banks around the world, which must now contend with a potential rebound in inflation. A 50% rise in the price of oil is a meaningful shock, and the resulting increases in gasoline, utility costs, fertilizer, and food prices have a real impact on consumer spending.

Now the Good News

While uncertainty surrounding the Iran conflict has weighed heavily on stock prices, investors still have reason for optimism. Wall Street analysts have continued to raise their earnings forecasts for companies in the S&P 500.

Despite the uncertainty that comes with conflict, the labor market has held up well. Unemployment claims have remained quite low, and the widespread layoffs that many feared have not materialized.

Recent losses in the stock market reflect growing unease over the Iran conflict, although investors may be finding some reassurance in the fact that political incentives tied to the U.S. midterm elections this year should motivate efforts toward a resolution.

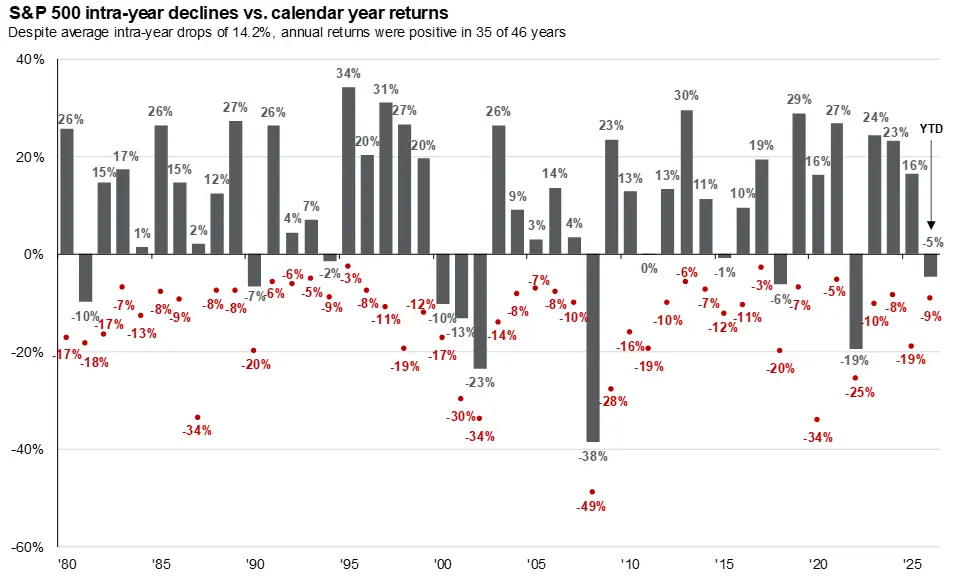

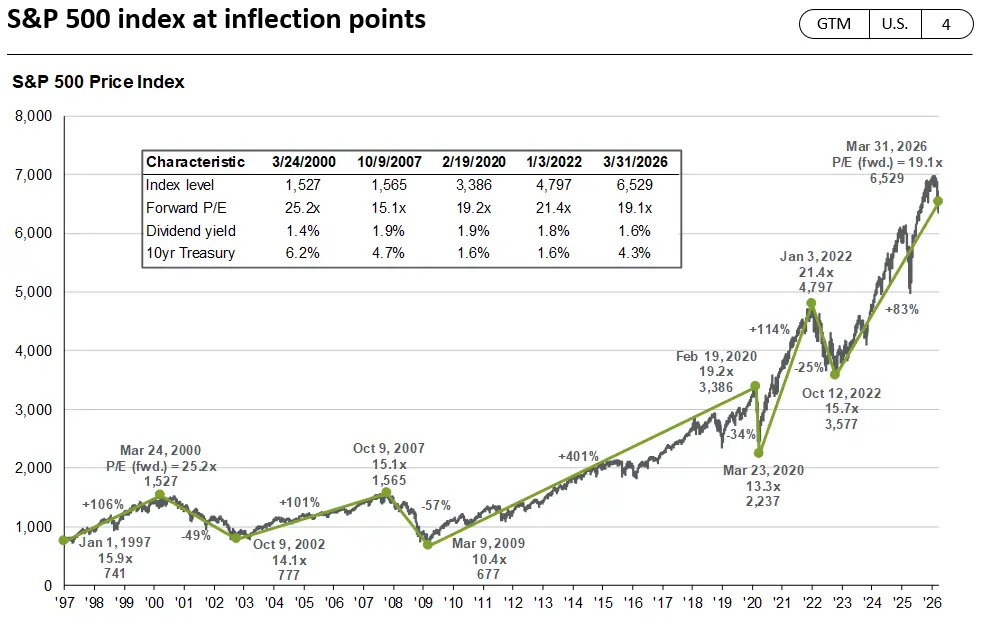

Overall, we see opportunities in the recent selloff in U.S. stocks. Growth prospects continue to improve, and the broader economic impact of the conflict has been limited so far. Historically, intense periods of market stress have been followed by economic recovery and lasting gains for the stock market. A year ago, the tariff shock from Trump’s Liberation Day initially rattled markets, as the historic increase was expected to raise the risk of a recession. But, that fear faded as markets rebounded at a remarkable pace, driven by strong corporate earnings growth and inflation that never materialized. We believe the 2026 energy shock will pass as well. History suggests that America’s ability to pivot, adapt, and adjust to adversity will prevail.

How We’re Positioning

In challenging times like these, we believe portfolios should be managed with discipline and diversification. U.S. economic fundamentals remain healthy, though uncertainty has increased. We caution against moving out of the market, as doing so may ultimately mean being on the sidelines when the recovery arrives. We favor conservative positioning across investments that are sensitive to growth and interest rates, with greater emphasis on maintaining flexibility and cash reserves during this period of extended uncertainty.

Within equities, we see opportunities in high quality technology software that sold off in January. The sell-off was driven by a narrative that AI agents would cannibalize the revenue model of traditional software giants. We believe the current environment represents a classic “sentiment-driven dislocation” where high-quality software is trading at a significant discount. We look for software businesses that own the proprietary data. For example, Intuit, the large tax software company, owns the “workflow real estate” that AI needs to live in.

During volatile markets, we continue to advise our clients into building portfolios with uncorrelated assets. Infrastructure is an asset class that we find attractive for most market conditions. Infrastructure is the essential backbone of the economy. Infrastructure assets can include utilities, toll roads, pipelines, data centers, cold storage, etc. Infrastructure is unique and, in many ways, behaves like a bond with growth appreciation. Though sensitive to a few factors that could adversely affect their business, including high interest costs in connection with capital construction programs, high degrees of leverage, and costs associated with governmental, environmental and other regulations, it is durable, with low volatility, inflationary hedge, predictable cash flows and low correlation with the stock market.

The Iran Conflict and Energy Markets

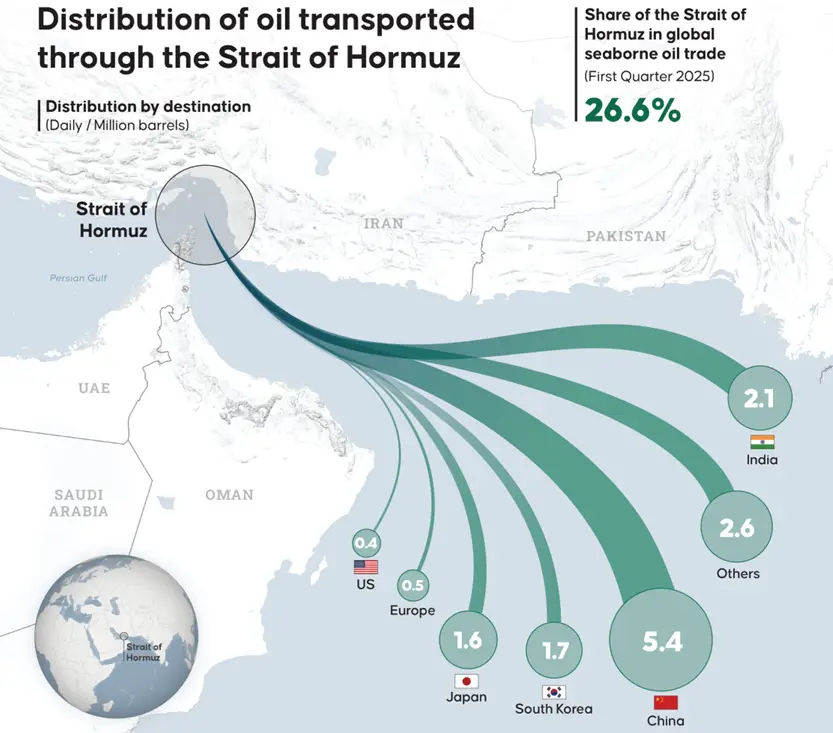

In recent years, financial markets have largely looked past geopolitical events. While energy prices typically spike during initial periods of stress, they have historically settled back down quickly. However, the situation following Operation Epic Fury — launched by the U.S. on February 28, 2026 — has been different. Iran has surprised many observers by attacking neighboring countries and declaring the “closure” of the Strait of Hormuz, a narrow 21-mile corridor between Iran and Oman through which roughly 20% of the world’s oil and liquefied natural gas flows2.

Asia is the most vulnerable, as 80% of the crude oil passing through the strait is destined for Asian markets3. On a relative basis, the Americas are the most insulated. Despite the near-term pain of higher domestic energy prices, the U.S. stands as the primary beneficiary of a global shift in energy supply, as countries seek to diversify where they source their energy. American liquefied natural gas (LNG) is the only supplier capable of filling the massive shortfall created by the damage to Qatar’s export facility.

Stock Market Outlook

Within the stock market, corporate America is expected to deliver strong first-quarter earnings results, although companies sensitive to oil prices and interest rates may strike a cautious tone until there is a resolution to the Strait of Hormuz closure and the broader Iran conflict. Assuming a resolution is reached, the economic impact should be limited. U.S. economic output is expected to grow at 2.5%, and favorable policy developments such as the One Big Beautiful Bill, massive AI investments driving corporate earnings, and stable employment all support a healthy outlook for the economy and markets. This remains our base case.

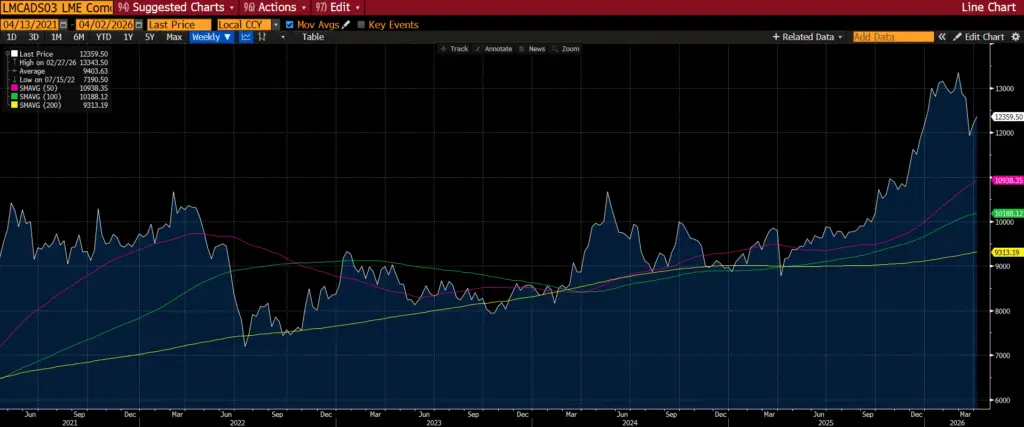

Copper is often viewed as a leading indicator for the direction of the economy. Copper prices dropped 9.5% in March, snapping a seven-month winning streak. The longer-term upward trend remains intact, but it will be important to watch whether copper can hold at current levels — doing so would likely signal stabilization and an improving backdrop.

The key risk in focus is that costs are rising while demand is weakening — the hallmarks of stagflation. The economy remains solid for now with strong demand, but it could become more fragile as supply is disrupted and inflation pressures build the longer the Strait of Hormuz remains closed.

Historical Copper Price (USD per Pound)

Bond Market

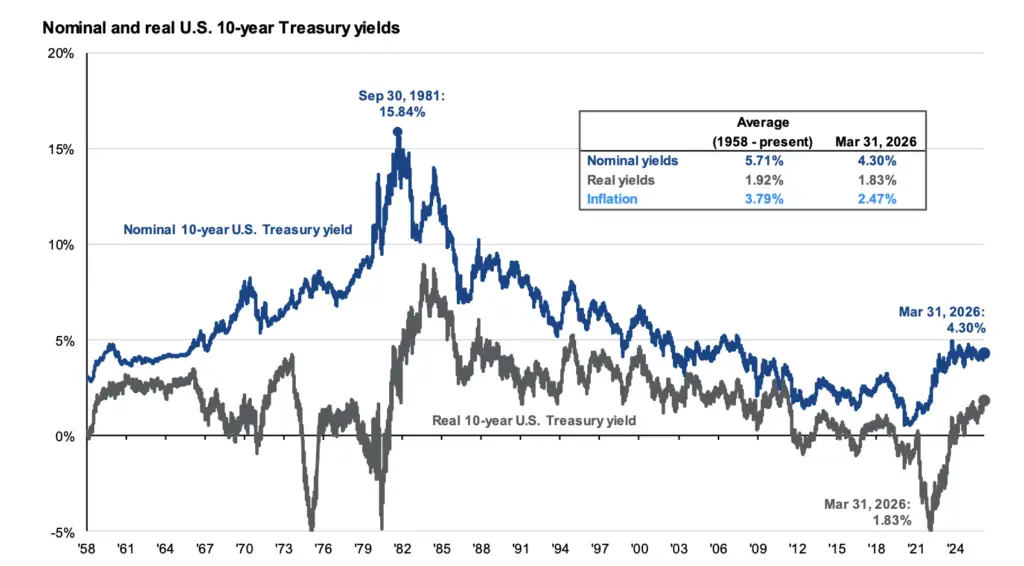

The bond market — specifically U.S. Treasuries — has not played its traditional role as a safe-haven during this period of stress. Yields have risen due to concerns about stagflation and the deterioration of the U.S. fiscal position.

We believe the bond market has priced in more tightening than is warranted. Our view is that the Federal Reserve remains on a path toward gradually lowering rates over the medium term. With this backdrop, we see bonds as attractively priced, and we expect higher-quality, longer-term bonds to perform well from here.

Sources

- Bloomberg provides all market and economic data, as of 03/31/2026

- https://www.bbc.com/news/articles/c78n6p09pznoInternational Development Markets benchmarked using MSCI ACWI-EX USA

- https://www.statista.com/chart/35914/destination-maritime-crude-oil-strait-of-hormuz/?srsltid=AfmBOopIYixnga56V3Ywwwa_Fj77jPjM2Alp_GTnQiIxIXreyYIWf_Fv

Index Definitions

Securities indexes assume reinvestment of all distributions and interest payments. Indexes are unmanaged and do not take into account fees or expenses. It is not possible to invest directly in an index. Indexes are all based in U.S. dollars. S&P 500 Index is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States.

Chicago National Activity Index is a monthly index designed to gauge overall economic activity and related inflationary pressure. University of Michigan’s Consumer Sentiment Index is a consumer confidence index published monthly by the University of Michigan. Nasdaq is an online global marketplace for buying and trading securities. New York Stock Exchange is a stock exchange where the equity shares of public companies are bought and sold.

Important Disclosures

Investing involves risk, including the possible loss of principal. Past performance is no guarantee of future results.

Channel Wealth and advisors do not provide legal, tax or accounting advice. Clients should consult their legal and/or tax advisors before making any financial decisions.

This information should not be construed as investment advice and is subject to change. It is provided for informational purposes only and is not intended to be either a specific offer by Channel Wealth or any affiliate to sell or provide, or a specific invitation for a consumer to apply for, any particular retail financial product or service that may be available.

All recommendations must be considered in the context of an individual investor’s goals, time horizon, liquidity needs and risk tolerance. Not all recommendations will be in the best interest of all investors.

Asset allocation, diversification and rebalancing do not ensure a profit or protect against loss in declining markets.

Investments have varying degrees of risk. Some of the risks involved with equity securities include the possibility that the value of the stocks may fluctuate in response to events specific to the companies or markets, as well as economic, political or social events in the U.S. or abroad. Investing in fixed-income securities may involve certain risks, including the credit quality of individual issuers, possible prepayments, market or economic developments and yields and share price fluctuations due to changes in interest rates. When interest rates go up, bond prices typically drop, and vice versa. Bonds are subject to interest rate, inflation and credit risks. Investments in high-yield bonds (sometimes referred to as “junk bonds”) offer the potential for high current income and attractive total return, but involves certain risks. Changes in economic conditions or other circumstances may adversely affect a junk bond issuer’s ability to make principal and interest payments. Treasury bills are less volatile than longer-term fixed income securities and are guaranteed as to timely payment of principal and interest by the U.S. government. Investments in foreign securities (including ADRs) involve special risks, including foreign currency risk and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are magnified for investments made in emerging markets. Investments in a certain industry or sector may pose additional risk due to lack of diversification and sector concentration. Investments in real estate securities can be subject to fluctuations in the value of the underlying properties, the effect of economic conditions on real estate values, changes in interest rates, and risk related to renting properties, such as rental defaults Alternative investments are speculative and involve a high degree of risk.

Alternative investments are intended for qualified investors only. Alternative Investments such as derivatives, hedge funds, private equity funds, and funds of funds can result in higher return potential but also higher loss potential. Changes in economic conditions or other circumstances may adversely affect your investments. Before you invest in alternative investments, you should consider your overall financial situation, how much money you have to invest, your need for liquidity, and your tolerance for risk.

Nonfinancial assets, such as closely held businesses, real estate, fine art, oil, gas and mineral properties, and timber, farm and ranch land, are complex in nature and involve risks including total loss of value. Special risk considerations include natural events (for example, earthquakes or fires), complex tax considerations, and lack of liquidity. Nonfinancial assets are not in the best interest of all investors. Always consult with your independent attorney, tax advisor, investment manager, and insurance agent for final recommendations and before changing or implementing any financial, tax, or estate planning strategy.

© 2026 Channel Wealth LLC,. All rights reserved.