Dear Investors,

We are pleased to welcome you to the new year and present our 2026 Market Outlook Report.

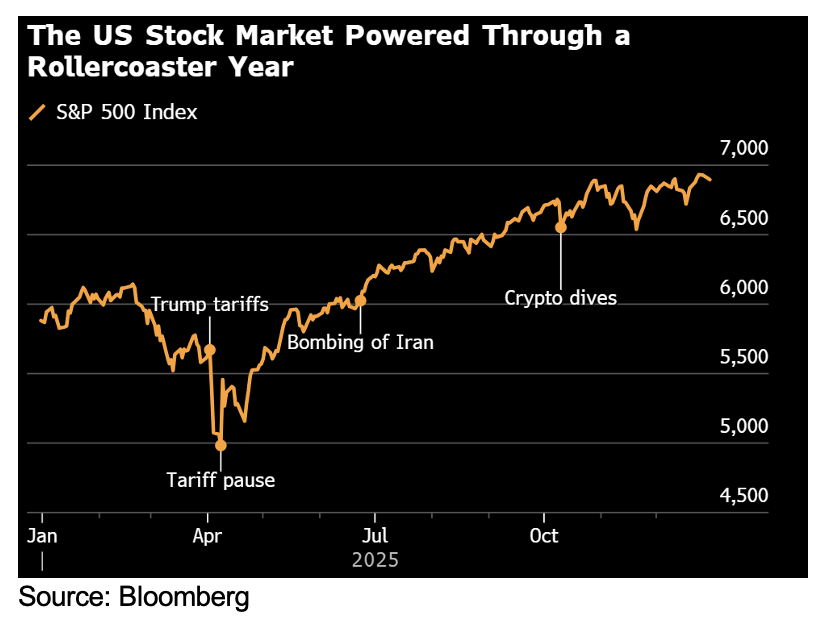

Closing out 2025, global stock markets delivered a spectacular performance. Despite initial volatility surrounding President Trump’s “Liberation Day” tariffs, the U.S. market rose like a phoenix, powered by robust corporate earnings. The S&P 500 gained 17.9% in 2025, marking its third consecutive year of double-digit gains1.

The “Magnificent 7” continued to provide a sturdy floor—rising 24.9%—the most notable trend of 2025 was the broadening of the rally. The remaining 493 companies in the S&P 500 returned a healthy 15.6%, signaling widespread market strength.

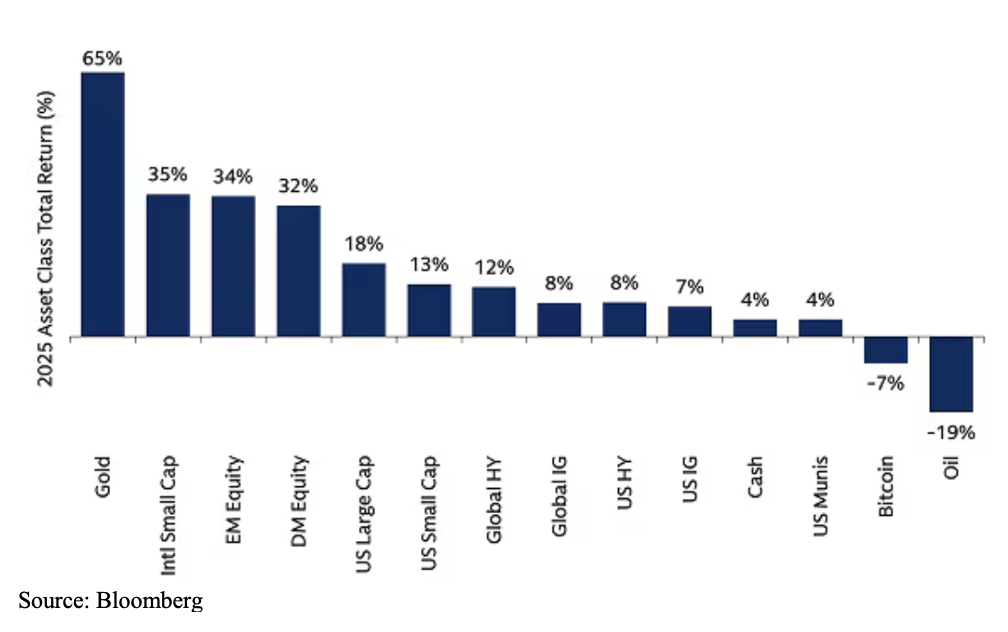

Gains were not confined to the United States. International markets rose 22% and precious metals recorded one of their best years in decades amid a rush to safe havens. Copper and rare earths were also standout performers, highlighting their geopolitical importance. Before a recent consolidation, cryptocurrencies were on track to beat equity returns for the year. Conversely, the major laggards for 2025 were oil and the U.S. dollar; oil headed for its deepest annual loss since 2020 due to oversupply concerns.

While there are certainly reasons for caution—growing national debt, inflation risks, and debates over AI stock valuation—we believe these are challenges for another year. In this letter, we recap 2025 and outline the opportunities we find attractive for 2026.

2025 Market Recap & Outlook: Turning Lemons into Lemonade

Earlier this year, the market was dealt a difficult hand. Between new tariff schedules, lousy consumer sentiment, a hawkish Fed, poor housing affordability, and a slowing economy, there were ample reasons for concern. However, Corporate America did what it does best: it adapted. After a shaky April, the Tech sector led a massive turnaround, setting a positive tone that eventually spread across the entire S&P 500 and international markets.

The results have been impressive. Not only did annual corporate profits surprise to the upside—rising 13% in the third quarter of 2025—but the economy also grew at a 4.3% annualized rate through October1. This is an astonishing feat considering we navigated a record-breaking government shutdown and growing skepticism regarding the strength of the AI rally.

International economies have weathered the global trade war surprisingly well in our view. International developed index returned more than 33.2%3, while emerging markets delivered a 34.3%4 return in 2025. The past year marked the end of a 15-year stretch in which foreign markets lagged behind the U.S1. The drivers for this outperformance included attractive valuations, the adoption of artificial intelligence, electrification themes, and improving financial conditions globally.

Equity Outlook for US & International Markets: We maintain our overweight on US equities as the market remains upbeat on 2026 corporate earnings momentum. One of the biggest and most surprising factors driving earnings is margin strength. Despite the uncertainties such as tariffs, large-cap

companies have been able to expand margins—a testament to both their agility and efficiency gains from innovation, including AI. Forecasts suggest profits will climb by another 15%1.

We believe overall market breadth should improve thanks to fiscal stimulus and some cyclical acceleration in traditional industries.

Outside the US, Japan and India have outpaced the U.S. earnings growth. Japan, and India markets have been driven by structural reforms and government spending in Europe. The global backdrop of lower US rates, and a weaker US dollar is supportive for international investing.

Positive Earnings Revisions in most regions

What does history say?

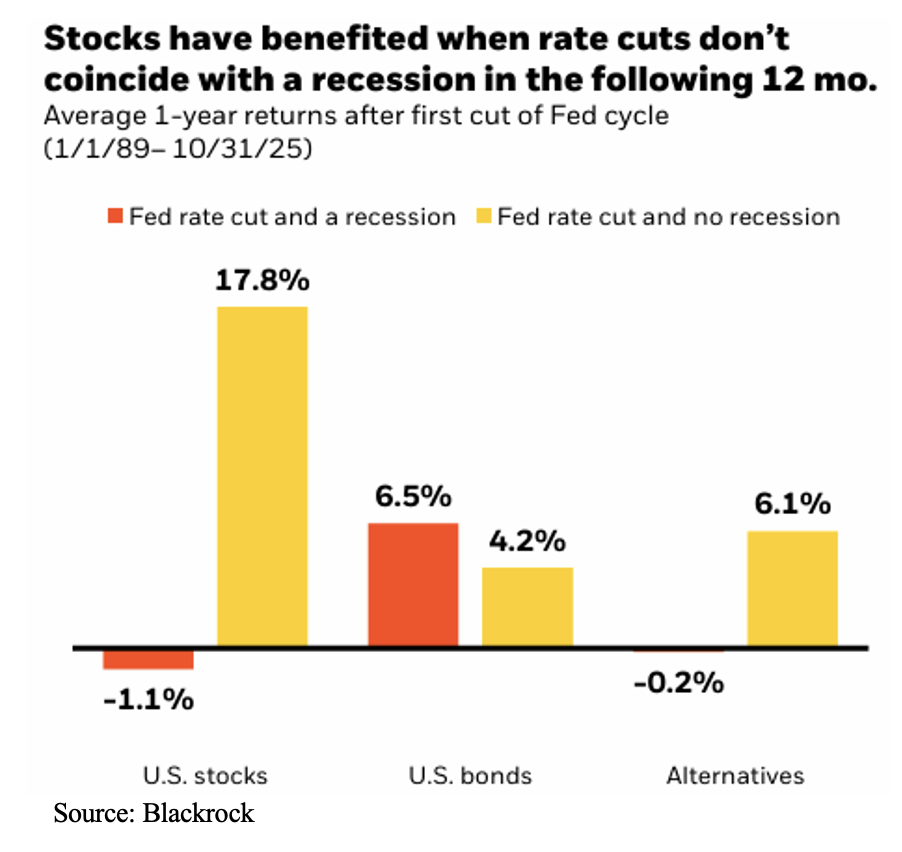

The combination of the 2nd year of a presidential cycle (the “Midterm Year”) and Federal Reserve rate cuts create an often-volatile environment for stock market. Historically, the 2nd year is the weakest of the four-year presidential cycle.

Conversely, when the Fed rate cuts to prevent an economic slowdown, (absent a recession) there are often above average returns the following year in the market. We see the first half of the year being more problematic for equity markets until midterm electionuncertainty clears. The second half of the year, we believe the market will likely generate most of its gains as rate cuts work their way into the economy.

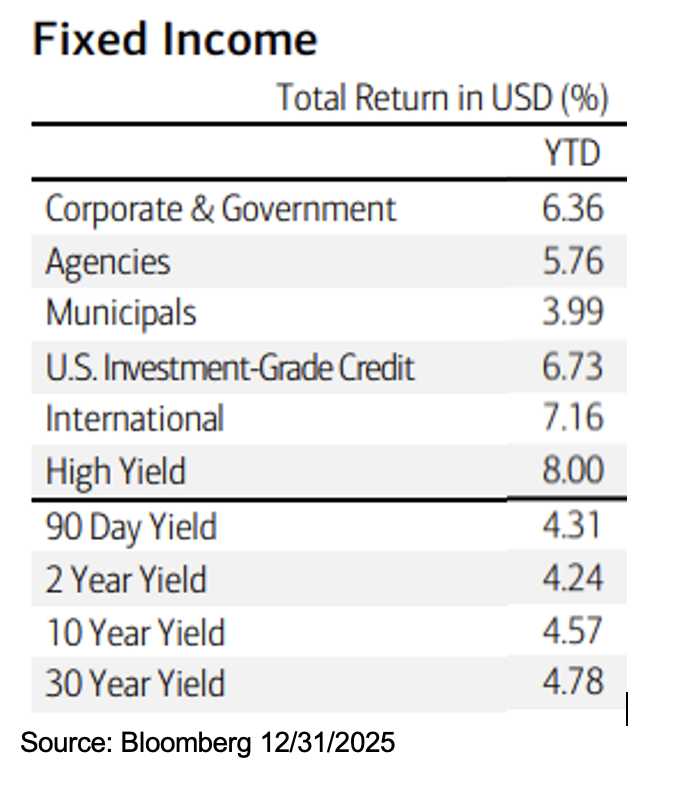

Fixed Income:

The Treasury market in 2025 delivered its best total return since 2020 as the Federal Reserve cut interest rates in response to weakening labor market conditions. Taxable bonds rallied aggressively earlier in the year as the economy cooled and the Fed signaled cuts. The municipal bond market did not participate in this early rally as it faced a “perfect storm” of technical and fundamental headwinds that caused it to significantly lag behind taxable counterparts like U.S. Treasuries and corporate bonds. While the Municipal bond asset class managed a rally late in the year to salvage positive absolute returns, the relative underperformance was driven by three primary factors: a historic surge in supply, legislative anxiety, and rich starting valuations.

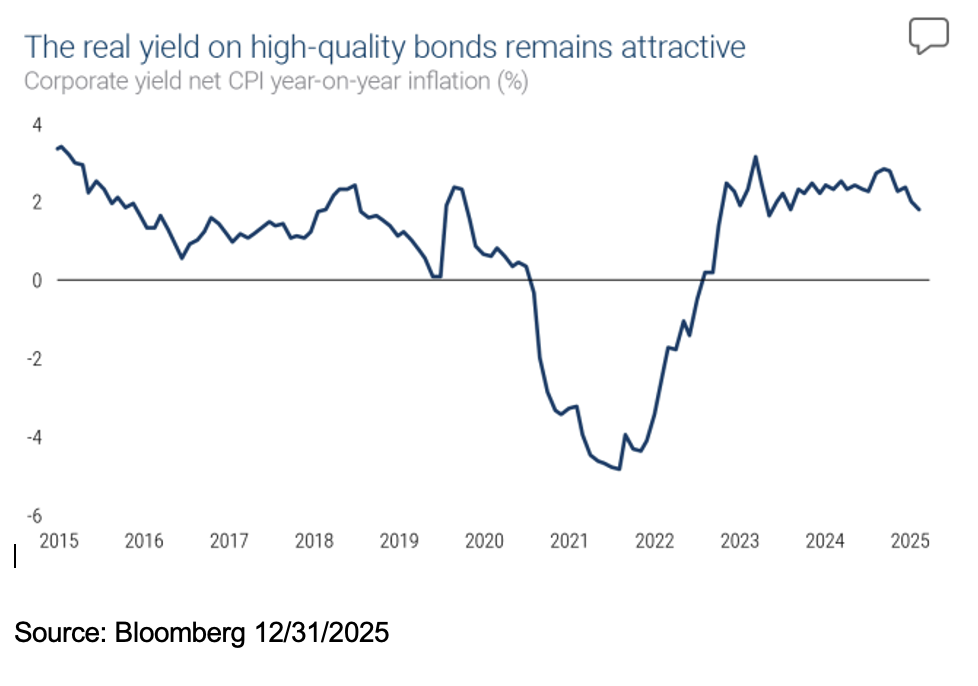

Fixed Income Outlook for 2026: We believe prospects for bonds continue to look strong. With proactive rate cuts by the Federal Reserve, resilient corporate fundamentals, and continued investor appetite for fixed income, conditions support compelling returns. Investment grade bond fundamentals appear solid, but credit spreads are relatively tight to treasuries.

We see 2026 shaping up to be a year where investors should be able to find value by extending duration and focusing on high quality global diversification. With 10-year Treasury yields around 4% and investment-grade credit yielding near 5%, investors can generate solid real income, especially with inflation hovering around 3%.

Commodities

Oil prices slid further during the 4th quarter, falling to a four-month low amid ongoing concerns about oversupply. Gold shattered expectations breaking through $4,000/oz barrier late in the year. While copper prices surged to all-time highs $12,000/ton driven by the data center and electrification A.I. buildout. Oil prices remained soft, averaging in the mid-$60s, driven by Non-OPEC supply flooding the market, while demand from China continued to soften to their high EV adoption rates. Given the massive infrastructure needs, we see industrial metals like copper with the highest upside in 2026.

Economic Summary – What you need to know

Economic resilience has been a key theme in 2025, and we think the setup for 2026 continues to be positive.

Several tailwinds support our optimistic outlook:

Businesses to immediately deduct capital expenses (R&D, equipment): The “One Big Beautiful Bill,” effective January 1, 2026, allows businesses to immediately deduct capital expenses (R&D, equipment). CBO analysis indicates this legislative change could lift GDP by nearly 0.9%2.

Corporate Profitability: After rising 13% in Q3 2025, corporate profits are forecast to climb another 15% in 2026. Globally, profits are set to rise 6-11%.

Monetary & Consumer Support: We anticipate lower interest rates, consumer tax refunds, and a weaker U.S. dollar to act as economic lubricants

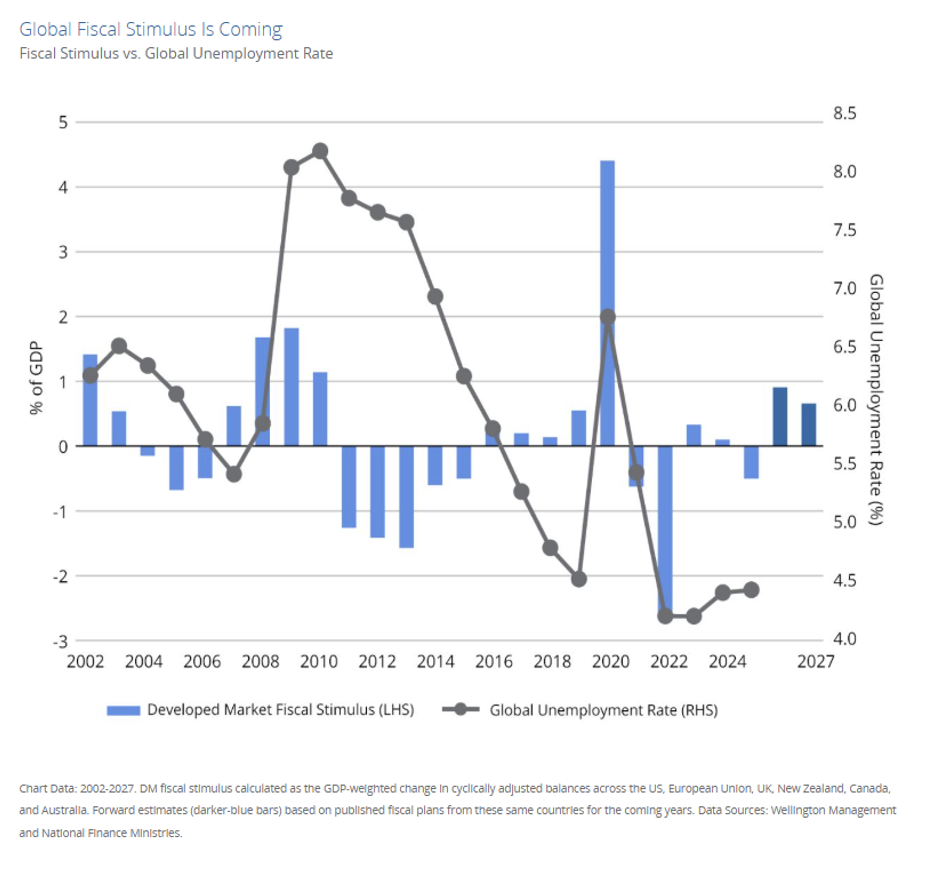

Global Fiscal Stimulus:

Every developed market region has planned fiscal stimulus that should support economic growth. This liquidity should drive business activity and economic growth.

In summary: We are optimistic heading into 2026. This positive stance is supported by four key pillars: the ongoing AI revolution, continued easing from the Fed, proactive fiscal stimulus, and a labor market that we expect to stabilize and begin a modest rebound.

Ultimately, successful investing in this cycle is about separating structural signals from market noise. As always, if you have questions about how these global shifts impact your specific situation, please do not hesitate to reach out. Thank you for your continued partnership.